Photo by AlphaGlider client, used with permission.

My youngest son graduates from college next month, and with that achievement comes new financial independence for him — and less cash outflow for my wife and me. Adulting can be daunting so my wife and I tried to progressively hand over fiscal responsibility to him throughout his high school and college years so that he would be better prepared for this moment. I have also fielded calls recently from several of my friends’ kids who are newly out of school and into the real world, and had questions about finances and investing. The following is the “Cliff Notes” edition of those conversations with my son and my friends’ kids. Feel free to pass these tips along to an emerging adult in your sphere, and perhaps these tips are good for all of us.

Resist lifestyle creep

Did you suddenly feel rich when you got your first paycheck or raise from your first professional job? I did. It can be so tempting to spend all of this newly found money on clothes, vacations, cars, toys, or a nicer apartment. The thing is, habits formed when you are young are hard to change as you age. Getting into the practice of living within your means early is essential for living within your means later in life.

Save early, save often

By living within your means, you are able to save early, buying you more time in the market. Time in the market is one of the most important determinants of the growth of an investment. The compounding of returns is a powerful thing.

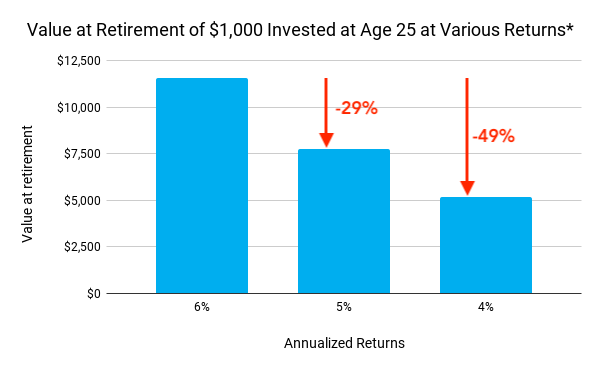

Source: AlphaGlider

*Key assumptions: 6% annual returns, 2.5% annual inflation, age 35 & 45 contributions adjusted upward for inflation, retirement age of 67

For example,1 $1,000 invested at age 25 grows to $11,557 at full retirement age (67) assuming a 6% annual compound rate of return. If you wait until 35 to make that investment (scaled up to $1,280 to account for 2.5% annual inflation to make a fair comparison), you get 29% less at retirement. And waiting to age 45, you are looking at 49% less.

But saving to invest should not come at the expense of investing in yourself, like going to graduate school or taking a lower paying job that will deliver experiences that could set you up down the road. Your first job will hopefully be the lowest paying job over your career, so do not sweat it if you are not able to begin saving substantial amounts in your 20s. Investing in yourself in your 20s is usually a good choice.

Minimize investment costs and taxes

If time is your best friend in investing, investment fees and taxes are among your worst enemies. Just as returns compound, so do expenses like investment costs and taxes.

The average fund2 management fee for equity and bond mutual funds is 1.12% and 0.82%, respectively (source: Investment Company Institute), an amount that comes out of your expected returns. So it is not a surprise to see that the average large-cap core fund underperformed its S&P 500^a benchmark by 1.54 percentage points annually over the last 20 years (source: S&P Dow Jones Indices; or by 35.8% total over this period). Maybe you think that you are above average and that you could pick fund managers who will outperform despite their high fees — but I would point out to you that only 1 in 18 large-cap core funds were able to beat its S&P 500 benchmark over the last 20 years (source: S&P Dow Jones Indices). Just do what AlphaGlider does and buy low cost, tax-efficient, indexed exchange-traded funds (ETFs), and lock in a return close to that of the index. For example, the total fund management fee for AlphaGlider’s balanced strategy (AG-B) is only 0.06%.

Another big investment fee to watch out for is the cost of a financial advisor, if you choose to use one. They typically charge about one percentage point (although AlphaGlider charges significantly less).

Source: AlphaGlider

*Key assumption: retirement age of 67

Adding up fund management and advisory fees, you can see how easily it can be to rack up over two percentage points in annual investment costs. Taking the earlier example of the 25-year old saver, an additional percentage point in expenses reduces their age 67 nest egg by 29%, as shown in the chart to the left. Two additional percentage points in expenses reduces it by 49%.

Minimizing, and/or deferring, taxes is a bit trickier, but one way is to be a buy and hold investor — i.e. a long-term investor. If you do not sell, you do not trigger taxes on realized capital gains in taxable accounts. In all types of accounts, minimizing trading reduces losses from the bid-ask spread. Another way to reduce taxes is to take advantage of tax-advantaged accounts like retirement accounts (e.g. 401(k)s, 403(b)s, traditional IRAs, Roth IRAs), college savings accounts (e.g. 529s), and health savings accounts (HSAs) when it makes financial sense.

“Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it. ”

Get to know Roth

On the topic of tax-advantaged accounts, a Roth IRA can be a particularly attractive long-term savings vehicle for young adults, especially if they are currently in a low tax bracket. Contributions made to a Roth are after tax, but after that there are no more taxes, including on eventual qualified distributions. This contrasts with a traditional IRA whose contributions are made before tax and their qualified distributions are taxed as income. As a general rule, one should contribute to a Roth IRA instead of a traditional IRA if their current tax bracket is lower than their expected tax bracket in retirement.

Let’s take the example of a 25-year old living in Texas earning $75,000, with $7,000 available to contribute to an IRA. Their income gives them a 22% marginal federal tax rate and because they live and work in Texas, they have no state income tax. In retirement they expect to have a 30% combined state and federal tax rate. With a Roth IRA, the young adult will be able to contribute $5,460 (the after-tax value of the $7,000), and it will grow to $63,101 by the time they hit full retirement age (67) assuming a 6% annual compound rate of return. Because it is a Roth IRA, the distribution is tax free.

Source: AlphaGlider

*Key assumptions: 6% annual returns, retirement age of 67

Now let’s see what happens if the young adult instead contributed to a traditional IRA. The full $7,000 would go into the traditional IRA as contributions are made before tax, and it would grow to $80,899 by age 67. However, they will be left with only $56,629 after paying taxes, 11% less than they would have received from the Roth IRA.

Another benefit of a Roth IRA is that contributions can be withdrawn any time without penalty or taxes. Distributions from a traditional IRA before the age of 59½ are charged a 10% penalty. Therefore, young adults should max out their Roth IRA contributions before putting funds in a taxable investment account, even if they think they may need to use the funds in the short to medium term.

The Roth “feature” can also apply to a 401(k) plan, excluding the bit about penalty-free early distributions. Therefore young adults usually find it advantageous to make all of their retirement contributions in their 401(k) plan to a Roth 401(k) account instead of to a traditional 401(k) account. Note that 401(k) plans were first allowed to add the Roth feature in 2006 and some plans have chosen not to add it. If the Roth feature is not allowed in your 401(k) plan, ask human resources to consider adding it, if only to better recruit and retain young employees.

Here is a link to an online calculator that can help you choose when its best to fund a Roth or a traditional retirement account:

Schwab Roth vs. Traditional IRA Calculator

Employer 401(k) matches are divine

Carrying on with our discussion of 401(k) plans, you should take full advantage of any employer match. It is free money that nearly always makes the total return on these contributions better than any where else you could deploy them. For many young adults, I recommend first maxing out 401(k) contributions that are matched by your employer, and then maxing out your Roth IRA. Additional savings could then either go to topping up your 401(k) or to a taxable account, depending on the timeline for the eventual need for those funds and your current and future expected tax brackets.

Note that employer matches of Roth 401(k) contributions are actually made on a pre-tax basis to a traditional 401(k) account, so you will eventually be taxed on them when they are distributed.

High yield savings for emergency funds

Everyone should have three to six months of liquid funds available to cover emergencies. Back in the 2010s when rates were low, it really did not matter where you kept these funds as you got close to nothing in interest in just about all accounts. However, that is no longer the case, with the exception of most checking and savings accounts (my bank still only pays 0.01% on both types of accounts!). Therefore I recommend holding only a little over one month’s expenses in your low yielding checking account, and the balance of your liquid emergency funds in an high yield online savings account. Do not hold any funds in your low yielding savings account and consider closing it down like I did last year.

A quick check on Bankrate shows several online high yield savings account options paying well over 5% at the moment. As your checking account grows and shrinks, you can move money between it and your high yield savings account to return the checking account to its optimal level of a little over one month’s expenses. Make sure that the high yield savings account is FDIC insured (most are; provides up to $250,000 coverage of your deposits should the bank fail). As you will be frequently moving money between it and your checking account, make sure that the high yield savings account does not have onerous minimum balances and restrictions on the number of monthly deposits and withdrawals, and that it has a mobile app that is easy to use.

Another good location for emergency funds is an I bond, available only at

TreasuryDirect. An I bond is even safer than funds at an FDIC insured bank, and it has the advantage of its interest not being taxed by the IRS until redeemed, and exempt from state and local taxes at all times. An I bond bought before the end of April will pay interest at an annual rate of 5.27% for its first six months. After that the rate goes floating (dependent of short-term inflation rates), but it is likely to be higher than that paid by high-yield savings accounts because it includes an additional 1.3% fixed rate that remains for the life of the I bond (note that I bonds bought after April will have a new fixed rate assigned to it). The main sticking point with an I bond, however, is that it cannot be redeemed until a year after purchase, and that you will forfeit the last three months of interest if redeemed within its first five years. But once you have held an I bond for a year, it is as liquid as any savings account and can be thought of as a fund for emergency expenses.

Diversify and set investment risk by time in market

Now that you know in which types of investment accounts to invest and which investment vehicles to use, it is time to discuss the assets in which you should invest.

The risk you take in your investments should depend on when you think you will eventually need to use those funds. Short-term funds should be invested more conservatively and long-term funds should be invested more aggressively. For example, those emergency funds which you may use tomorrow or next month need to be there with a high level of certainty, thus they should be invested conservatively. Your returns won’t be spectacular, but that is less important than the fact that you know that they will be there if and when you need them.

On the other end of the time spectrum would be your retirement savings, which a young adult may not need to use for another 45-65 years. These investments should be invested aggressively so as to take advantage of the higher long-term returns expected for taking on more risk and volatility. Below is a chart of returns for US stocks (S&P 500; high risk), US corporate bonds (intermediate risk), and 3-month Treasury bills (low risk) over the last 95, 50, and 10 year periods — showing that the more risk you take, the higher return you should expect over long time periods.

Source: Barbara Friedberg with data from Aswath Damodaran

It is important that once you set up your long-term aggressive investments, that you stick with them. You will inevitably see some ugly years of performance over the coming decades that may make you want to bail out, but that is usually when future expected returns are their brightest. Rest assured in the previous chart. Resist the temptation to buy high and sell low. If you do not think you will have the stomach to stick with aggressive investments in your long-term accounts, then consider finding a financial advisor who has a long-term outlook.

Diversification of your investments is also important. I will not go through the math here (but Nobel Prize laureate Harry Markowitz does in his seminal paper entitled Portfolio Selection), but diversification allows you to increase your expected returns at a given level of risk taken. In practice, a young adult can diversify their aggressively positioned retirement accounts with equities from multiple regions, industries, and valuations. As one grows older and closer to the time that they will need their savings, other less aggressive asset classes (e.g. bonds, commodities, etc.) should increasingly be added to both lower investment risk and increase diversification. Owning index funds, as opposed to individual stocks, adds to diversification due to the shear number of companies held.

Insure to ensure and assure

Adulting is expensive and you may feel tempted to cut corners by foregoing insurance or by underinsuring. Please don't. Just as with your investments, protect your downside risks.

You have a long life in front of you, and it would be a shame if you let a random event put you in a position that will be hard to come back from. Also, it would not be fair to your friends and family who may feel obliged to financially bail you out of an expensive predicament brought on by your lack of insurance.

What insurance are we talking about? Health insurance for sure. Auto insurance too, as it's the law. And even if your car may not be worth that much, the car you crash into may be and there's also personal injury costs to consider. Renters insurance is cheap and you may be surprised at how much it would cost to replace all of those clothes and electronics. Renters insurance can also protect you should your new dog bite someone. When you get older and have others relying on you financially, consider disability and life insurance. And if you are fortunate to build a large nest egg, I recommend getting an umbrella policy to protect you from large claims or lawsuits that go above your other insurance policies.

Protect your credit score

My final bit of financial-related advice to these young adults is to protect their credit score. A weak credit score can cause all kinds of problems such as making it harder to rent an apartment, paying higher rates on insurance (e.g. car, renters, homeowners), being rejected on a personal loan (e.g. car, home) or paying higher interest rates on it, and even cause you to lose a job offer from a prospective employer. Basically, your credit score is a three-digit indication of how responsible you are to these important counterparties.

How do you protect your credit score?

- Pay your bills on time

- Pay off your credit card balance monthly. If you are living within your means and have your emergency funds built up, this should not be a problem.

- Protect your identity like your credit score depends on it, because it does:

- Use biometrics on your smartphone (e.g. fingerprint and facial recognition)

- Use unique strong passwords for every online account you maintain (a password manager is vital)

- Use two-factor authentication (2FA) when available

- Place a security freeze on your credit report with each of the three major credit reporting agencies.

Summary

Adulting really isn't that hard. Definitely not as hard as navigating high school and college. Yes, there are a lot of new terms, but the concepts are quite simple and intuitive. Just keep it simple, don't procrastinate, and keep engaged and learning about personal finances. You'll be fine.

**NOTES & DISCLOSURES**

1This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor.

2Mutual funds, exchange-traded funds and exchange-traded notes are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained directly from the Fund Company or your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

^Indices are unmanaged and investors cannot invest directly in an index. The performance of indices do not account for any fees, commissions or other expenses that would be incurred.

aThe Standard & Poor's 500 (S&P 500) Index is a free float-adjusted market capitalization weighted index that is designed to measure large cap US equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization in the US equity markets.

Copyright © 2024 AlphaGlider LLC. All Rights Reserved.

No part of this report may be reproduced in any manner without the express written permission of AlphaGlider LLC.